Table of Content

That’s not to say that the risks of a home equity loan aren’t worth taking; in some cases, a home equity loan can be a good idea, especially if you use the funds to renovate your home. Because interest rate increases are unpredictable, HELOC borrowers could end up paying much more than they originally signed up for. Lenders will usually allow you to borrow up to 80% of your equity with a cash-out refinance and between 80 to 90% of your equity with a HEL or HELOC. Home equity loans are often commonly referred to as second mortgages because you effectively have 2 loans taken out on one home.

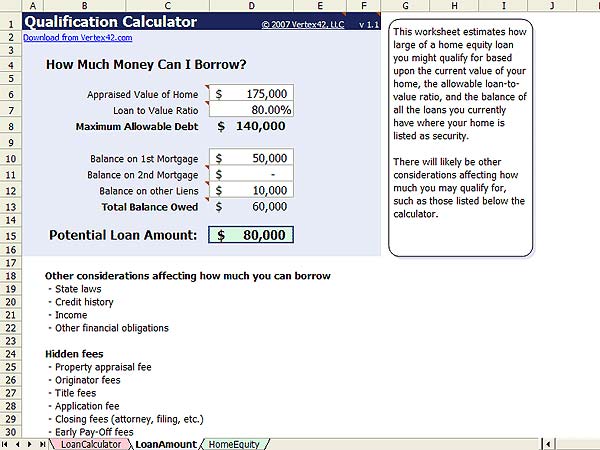

Credit bureaus recommend you keep your revolving balance under 30% of your credit limit. That presented a major problem when HELOCs became popular in the 1990s. HELOCs are classified as a revolving type of credit on most credit reports, the same designation as credit cards. Theres also a limit to the amount you can borrow on a HELOC or home equity loan. To determine how much money youre eligible for, lenders will calculate your loan-to-value ratio, or LTV. Even if you have $300,000 in equity, the majority of lenders will not let you borrow that much money.

What Are Home Equity Loans and HELOCs?

Freezes can happen when you need the money most, and they can be unexpected, so the flexibility comes with some risk. You can borrow a fair bit of money if you have enough equity in your home to cover it. If you think your lender has violated the law, you may want to contact the lender or servicer to let them know. If the required notice and disclosures are not provided, you may have up to three years after opening the plan to rescind the HELOC. Avoid a lender who wants you to apply to borrow more than the amount you need. It’s Cyber Security Awareness month, so the tricks scammers use to steal our personal information are on our minds.

The amount of money you can withdraw from your home depends on your current loan balance and the value of your home. If youre self-employed, youll have to provide your federal income tax returns for the last two years. If you receive retirement income, the lender will want to see a retirement award letter or 401 distribution letter. You might be able to deduct the interest paid on home equity loans for home improvement from your taxes. Consult your tax advisor for more information about your specific circumstances.

Costs of a Home Equity Loan

You get the loan for a specific amount of money and it must be repaid over a set period of time. You typically repay the loan with equal monthly payments over a fixed term. If you don’t repay the loan as agreed, your lender canforeclose on your home.

Learn to change your habits when it comes to credit cards and debt. Make a written plan to pay off your debt that doesn't involve putting your house on the line. With mortgage rates what they are, a lot of people are taking stock of their home equity, says Persaud. But remember, borrowing with home lending products comes with some serious risks.

Pros and Cons of Home Equity Loans

If this happens, you could talk with your lender and try to restore your line of credit, or shop around for another mortgage to pay off your prior line of credit and get another one. During this three-day waiting period, the lender cannot directly or through another person take action related to the loan. The lender can’t deliver the money for the loan , or begin performing services. If you’re getting a home improvement loan, the contractor can’t deliver any materials or start work.

It's possible to get more than one home equity loan on your house, but it can be difficult. You'll need to have enough equity in your home to support your primary mortgage and multiple additional loans. Additionally, many lenders won't want to be third in line for repayment if you run into financial troubles. The best lender for you can depend on your goals and your needs.

So if the closing happens on a Friday, and if that was the last thing to happen, you have until midnight on Tuesday to cancel. For cancellation purposes, business days include Saturdays but not Sundays or legal public holidays. You can cancel for any reason,but only ifyou’re using your main residence as collateral. The right to cancel doesn’t apply to a vacation or second home.

Justin Pritchard, CFP, is a fee-only advisor and an expert on personal finance. He covers banking, loans, investing, mortgages, and more for The Balance. He has an MBA from the University of Colorado, and has worked for credit unions and large financial firms, in addition to writing about personal finance for more than two decades. Have low monthly payments, but a large lump-sum balloon payment due at the end of the loan term. If you can’t make the balloon payment or refinance, you face foreclosure and the loss of your home. If you’re thinking about getting a home equity loan or a home equity line of credit, shop around.

Maurie Backman writes about current events affecting small businesses for The Ascent and The Motley Fool. Both a home equity loan and a HELOC let you borrow against your home. A home equity line of credit is a type of home equity loan that has a revolving line of credit.

When you borrow with a home equity loan or HELOC, you use the difference between your home’s value and what you owe on your mortgage as collateral. Since they are secured loans, you can often get a more competitive rate with a home equity loan or HELOC than with, say, a personal loan. These mortgages are tailor-made for homeowners age 62 or older, particularly those who have paid off their homes. Although you have a few options for receiving the money, one common approach is to have your lender send you a check each month, representating a small portion of the equity in your home.

Home equity loans almost always have a fixed interest rate, meaning your monthly payment won’t change as rates bump around. The average annual interest rate for a home equity loan is around 6%. Some lenders offer lower rates if you let them auto draft your payments from your bank account. But you’re only catching a small break—you’ll still pay plenty of interest over the years. Home equity—the current value of your home minus your mortgage balance—matters because it helps you build wealth. When you have equity in your home, it’s a resource you can borrow against to improve your property or pay down other high-interest debts.